The Covid-19 pandemic has stirred up confusion in so many aspects of life! The turmoil in the markets over the past few months, combined with the uncertainty of what might be ahead, has definitely made some changes in how we make financial decisions.

One of the ways your finances may have been affected by this shakeup is how to plan for your retirement and manage your money toward your goals. After all, your situation in life might have taken a complete 180 with regard to your income. And what was once viewed as a wise investment decision before the pandemic, may be viewed as riskier today.

If you’re wondering whether Covid-19 should bring changes to your retirement plan, you have several things to consider.

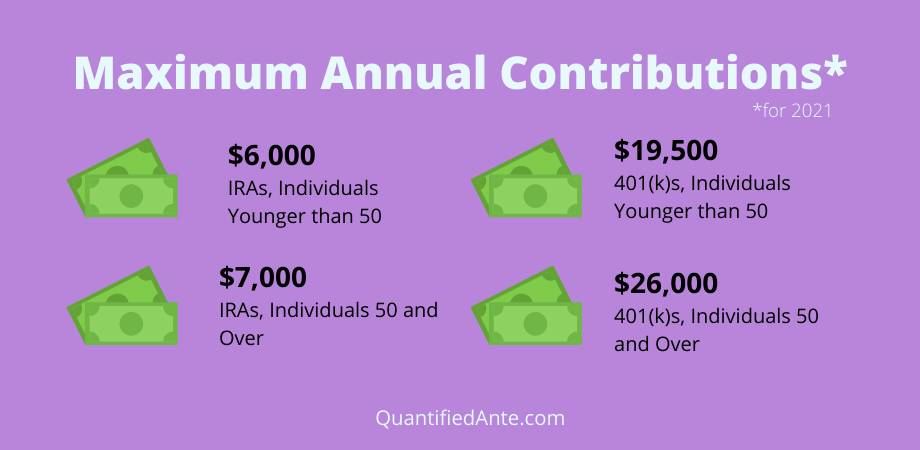

How Much to Put Toward Your Retirement Account

A key part of retirement planning is allocating how much you want to contribute regularly to your retirement accounts like IRAs or 401(k)s. If you’ve already mapped out a budget for retirement savings that includes monthly contributions, you may be wondering whether you should change the amount you contribute as a result of the effects of Covid-19.

The answer depends in part on how Covid-19 has affected your life, particularly your regular income. Aiming to stay on track with your retirement savings goals should be a top priority, but it’s not always feasible to save what you’d like when your life circumstances change.

If you have continued to work in your job and have very little reason to believe your job is in jeopardy as a result of the economic effects from Covid-19, you can probably continue to save as you originally planned and manage your credit accordingly.

Even if your employer has stopped offering matching contributions, you can still aim to keep your retirement savings on track by continuing to have your 401(k) contributions automatically deducted from your paychecks. That way, you stay in the healthy habit of saving and continue to build your nest egg.

You might even want to consider saving more these days, if possible, to prepare for a more uncertain future. That’s especially true if you’ve found that the Covid-19 pandemic has actually allowed you to cut costs – for example, commuting expenses if you’ve changed to working from home or restaurant expenses if you’re eating out less and eating more affordable meals in your kitchen. You might find you can put more toward retirement to create more security.

Managing Retirement Savings if You Lost Your Job

If you lost your job or if you are afraid you might lose your job soon, you may be forced to reduce your retirement savings contributions so that you can pay for life’s necessities. You need food and shelter, along with basics like electricity and heat. You also need to ensure you have health insurance because, without it, you risk major costs from an unexpected event that could put you into bankruptcy. So, without a job, you may simply no longer have enough income to contribute your regular retirement savings allotments.

Part of whether you will be able to stick to your budget will depend on:

- Whether you’ve built up emergency savings.

- How long that savings can fund your lifestyle.

- Whether you can land a new job soon.

As a general rule of thumb, it’s best to tap into retirement savings to pay for your life necessities only as a last resort. When you take money out of a retirement account early, you risk losing tax advantages, having to pay a hefty fee, and not saving enough to retire as you planned.

In desperate cases, using retirement funds may be your only option. Part of Covid-19 relief efforts have included more lenient rules about using 401(k) loans, which allows you to borrow against the money you saved in your 401(k) and repay it over five years. Again, though, this should be considered a last resort after tapping other sources like emergency funds and cutting back on your living expenses as much as you can before turning to your retirement savings. If you do have to use retirement funds, you may have to revisit the timeline for when you plan to retire, and perhaps consider planning on retiring later.

Again, what works for you will depend on your specific financial situation. Turning to a financial advisor who can review the pros and cons of making changes to your retirement plan would be a wise move.

Should You Change Your Retirement Accounts Asset Allocation?

Establishing your portfolio’s asset allocation is another important part of retirement planning. The way you allot a certain percentage of your portfolio to particular assets helps you develop a portfolio that aligns with your risk tolerance so you can achieve your goals, whether that’s making a higher profit or preserving your money.

Revisiting your asset allocations during a pandemic is important because the market can undergo some crazy swings. Your allocations could easily get out of whack, so you might want to rebalance more often.

During times of crisis, you may find that your risk tolerance is much lower – that you want to protect your assets in a much more conservative way. You may find that some of your assets have a new risk profile – industries or sectors that once were considered safe may now be viewed as more of a risk. For example, you may now consider stocks of companies in the restaurant and tourism industry to be riskier assets because this sector has taken a hard hit during the past year, and the future of that industry is uncertain.

I’m not here to make specific stock recommendations for you – or even help you with your exact investing decisions. What I want to do is to point out that there are key factors that can influence how you shape your retirement plans often change during chaotic times like we’re seeing during this Covid-19 pandemic.

A New Kind of Crisis

The kind of changes that Covid-19 have brought on is vastly different than the ones we’ve seen in previous economic crisis. These days, many of the changes in the economy are driven by the federal government’s decisions on how to best provide economic relief.

As an Investopedia article points out, “the current economic crisis isn’t driven by financial fundamentals, but by society’s deliberate effort to control the spread of the virus by shutting down large parts of the economy.”

New stimulus packages can provide short-term boosts for investors, but you need to be aware that they may have longer-term consequences that can affect your retirement portfolio. For one, stimulus packages are designed in a way that can cause inflation, and that can mean the value of U.S. currency can decline against other currencies. So, if you have a lot of cash reserves, you might want to factor in the possibility that your cash could lose value.

Government efforts to boost the economy have also fueled lower interest rates, which could have a number of impacts on your portfolio.

Of course, going into the crisis we were already seeing very low-interest rates, which meant we saw lower rates on bonds and savings accounts, among other effects. New policies may mean that lower rates are here to stay longer. These are things to think about as you revisit your retirement plan.

The Bottom Line

Life constantly changes, and no one knows how long this pandemic will last – nor how long its economic effects will last. So, it’s a good idea to review your investing plans – including your retirement investing plans — and make sure that your goals are in place and your strategy matches your goals.

Now that you have a better sense of the pandemic’s role in retirement planning, you can turn to a financial advisor who can sit down with you and go over your own plans and retirement goals. That way, you can make better decisions about how to develop a retirement plan that fits your current financial situation and puts you on track to the retirement you envision.

Hope You Enjoyed the Read!

Can you be more specific about the content of your article? After reading it, I still have some doubts. Hope you can help me. https://www.binance.com/fr/register?ref=S5H7X3LP

Thank you for your sharing. I am worried that I lack creative ideas. It is your article that makes me full of hope. Thank you. But, I have a question, can you help me?